Is the faucet leaking, or do you need to mail in a late rent check? You might just end up placing a call to your local bank.

Banks becoming landlords is the latest fallout from the real-estate bust. It's a decision few banks have pursued locally or nationally, but some in the banking industry say it could pick up steam as financial institutions tire of fire-sale prices on foreclosed properties.

The move got a boost last month when federal regulators issued new guidance that gives banks more flexibility to rent properties as a way to stem the flow of foreclosed homes hitting the market in unprecedented numbers.

“I think it's too early to see how popular it will be,” Julie Stackhouse, senior vice president of the Federal Reserve Bank of St. Louis, said of banks turning foreclosed homes into rental properties.

People are also reading…

Still, rentals might help a bank. Current trends in the rental market are favorable and the move could stabilize home prices in certain neighborhoods, which in turn would allow a bank to recover more money, according to Stackhouse.

“The demand for rentals is up,” she said. “Using rentals for a period of time allows an area to return to a more normal environment.”

Unimpressed with low offers on homes it owns, Clayton-based Truman Bank is waiting out the down real estate market and renting dozens of foreclosed properties in its portfolio.

Erik Beishir, Truman's president and CEO, said the bank's long-term goal is to find buyers for the properties, but that the bank is willing to undergo the headaches of being a landlord for the short-term.

“We as bankers are not in the business to be landlords,” he said. “But the folks who are buying homes right now are still looking for a bargain. We can't afford to sell at a bargain price.”

For Truman, which has four local branches, that's meant taking monthly rental checks and seeking qualified renters for the nearly 100 homes it owns in region whose prior owners defaulted on loans. Forty-six of the those homes have renters living in them.

It's unfamiliar territory for the bank, which isn't used to responding to calls for home repairs and other myriad responsibilities that come along with being a landlord.

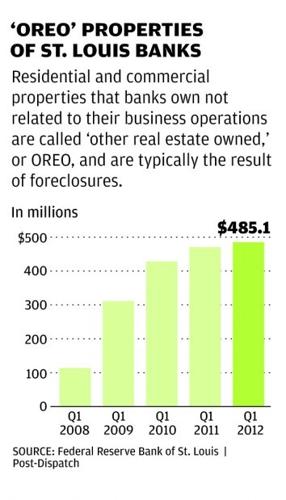

To keep up with the new responsibilities, Truman Bank hired two staff members recently to manage its rental properties. The bank has more than $30 million in 'other real estate owned' or OREO properties in its portfolio, three times the amount it had two years ago. Truman -- which has struggled with high levels of commercial and residential real estate loans that went into default -- has been warned by regulators to clean up its bad loans and boost its capital levels.

For all St. Louis-chartered banks, the amount of OREO properties quadrupled since the onset of the financial crisis, jumping from $113.6 million in the first quarter of 2008 to $485 million this year, which may signal that more bank-owned homes will convert to rentals.

NEW GUIDELINES

In better economic times, regulators encouraged banks to sell OREO property quickly. Banks are limited by state and federal regulations on how long they can retain ownership of residential properties – a maximum of five years unless they receive an extension.

But as the number of foreclosed properties has ballooned – as of last September, commercial banks in the U.S. had $10 billion in residential OREO properties according to the Federal Reserve – regulators have looked for ways to offer relief to the weakened housing market.

In April, the Federal Reserve provided an updated policy statement that provided guidance to banks seeking to rent homes. In the statement, the Fed said banks should still make a good faith effort to sell homes they own at the earliest practicable date. But the Fed also gave banks some leeway, saying that, given the current extraordinary market conditions banks can rent residential OREO properties “within legal holding period limits without demonstrating continuous active marketing of the property for sale.”

That new guidance prompted a few bank representatives to call the Missouri Bankers Association to check on the ramifications of renting in recent weeks, said the association's president and CEO Max Cook.

“It may make sense on a selected basis for banks,” Cook said.

Many of the largest banks that operate locally, including U.S. Bank and First Bank, said they have no plans to rent homes. But some banks are dipping their toes in the rental market. Bank of America launched a pilot program in March, called Mortgage to Lease, for customers facing foreclosure to stay in their homes and pay rent instead of a mortgage. Under that program – which is only available in New York, Arizona and Nevada – customers surrender their title to the property and their mortgage debt is forgiven. A Bank of America spokeswoman declined to divulge the level of interest in the program since it launched or whether it will be rolled out to other states. “We are reviewing the results and will determine next steps accordingly,” said spokeswoman Jumana Bauwens.

Bob Davis, executive vice president of mortgage market policy for the American Bankers Association, said he views the Fed's policy statement as a positive for the banking industry.

“Anytime regulators indicate a little more flexibility with a problem situation, that's good,” he said.

Davis said he expects more banks to pursue rentals but said most banks will still prefer to stay out of the landlord business.

“The regulatory action will result in more banks renting,” he said, “but most institutions will conclude that they're better off not being property managers.”

The Missouri Bankers' Association's Cook agreed, and said the costs associated with insuring and maintaining homes and collecting rent payments will deter many banks from pursuing rentals.

"My guess is that it won't grow much,” Cook said. “Banks are in the lending business, not the landlord business.”

Read more from Lisa Brown, who covers banking, consumer products and legal affairs for the Post-Dispatch. Follow her on Twitter @lisabrownstl and the Business section @postdispatchbiz.