It is not uncommon to see solicitations for business on social media websites — for many industries, social media advertising and digital marketing are common practice. However, such advertisements in the mortgage industry may end up costing the company penalty fees in violation of the Real Estate Settlement Procedures Act of 1974 (RESPA). Section 8 of RESPA, which became effective on June 20, 1975, focuses on prohibitions for kickbacks, fee splitting and unearned fees.

It continues to be a highly enforced provision by the regulators, with their increased effort focused on protecting the consumer. Specifically, this section of the statute prohibits anyone from giving or accepting a fee, kickback or anything of value in exchange for referrals of settlement service business involving a federally related mortgage loan. In addition, RESPA prohibits fee splitting and receiving unearned fees for services not actually performed.

As the original supervisory agency, the Department of Housing and Urban Development administered and enforced RESPA along with Section 8 of the Act until July 21, 2011, when the Consumer Financial Protection Bureau took the reins of enforcement. Once the CFPB took over and became the supervisory entity for Section 8, a few changes occurred. Some changes focused on the logistics of the CFPB and how enforcement is handled, while other changes brought along new rules altogether.

Social Media Addition to RESPA

RESPA Section 8 guidance regarding fee solicitation and kickbacks was supplemented in December 2013 when the Federal Financial Institutions Examination Council issued a Social Media Guidance and the CFPB issued rules to complement the FFIEC’s guidance. With the advent and increasing popularity of social media, it is very easy for financial institutions to attract customers with a Facebook post or Twitter tweet. Since a primary concern by these regulating agencies is consumer protection, the rules and guidance were implemented to address a potential for increased harm to the consumer, along with likely compliance and legal risks that companies could experience as they venture into this new avenue of social media as a means for business generation.

The guidance defines social media as a form of online communication where users can generate and share content through text, audio, video and/or images. It also specifically lists social media sites including Facebook, Google+, Twitter, Flickr, Yelp, YouTube and social media games such as FarmVille and CityVille. The guidance was careful to distinguish stand-alone email and text as not constituting social media.

The guidance defines social media as a form of online communication where users can generate and share content through text, audio, video and/or images. It also specifically lists social media sites including Facebook, Google+, Twitter, Flickr, Yelp, YouTube and social media games such as FarmVille and CityVille. The guidance was careful to distinguish stand-alone email and text as not constituting social media.

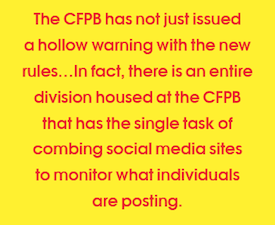

The CFPB has not just issued a hollow warning with the new rules. The agency has been implementing plans to use social media to track down individuals and companies who have been violating Section 8 via the subject matter of their online social media posts. In fact, there is an entire division housed at the CFPB that has the single task of combing social media sites to monitor what individuals are posting. Regulators are searching for violations by title companies, real estate agents and developers by searching for buzz words, such as “referral” and “referral fee.”

Some companies have loan officers that are posting on social media sites such as Facebook and LinkedIn. These posts are generally advertisements for cash or gift cards in exchange for referrals, with additional monetary compensation upon such referrals leading to the closing of a loan. While this may seem like an innocent ploy to generate business, such fees are not permitted to be paid out or collected for a service that has not yet been performed.

With a simple post online, the loan officer is subjecting himself, the employer or both to a violation of Section 8 of RESPA. This, in turn, can lead to civil and criminal penalties, negative publicity and a damaged reputation for both the individual and the company.

Consequences of Violating Section 8

RESPA Section 8 was created with the intention to help consumers become better shoppers for settlement services and to eliminate kickbacks and fees, which may increase the price of settlement services. The consequences of violating Section 8 include civil and criminal penalties.

Criminal penalties by a person in violation of Section 8 can result in up to one year in prison and a fine not to exceed $10,000. Any person in a civil lawsuit regarding violation of Section 8 is jointly and severally liable to the person charged for the settlement service an amount equal to three times the amount of the charge paid for the service. Individuals have one year to bring a private lawsuit to enforce violations of Section 8. Private lawsuits may be brought in any federal district in which the property is located or the violation occurred. Furthermore, the state attorney general, HUD, or state insurance commissioner may bring an injunctive action to enforce violations of Section 8 within three years of the violation.

Recently, the CFBP took action against two of the nation’s largest banks for illegal mortgage kickbacks. Both institutions were found to have been aware of their loan officers referring homeowners to a now defunct title company in exchange for cash, marketing materials, and consumer information. Collectively, the banks will pay $35.7 million in civil penalties, while the loan officer who generated the largest amount of kickbacks must pay $30,000 in civil penalties.

“These banks allowed their loan officers to focus on their own illegal financial gain rather than on treating consumers fairly. Our action today to address these practices should serve as a warning for all those in the mortgage market,” said CFPB Director Richard Cordray.

A third financial institution was found to have loan officers that participated in this kickback scheme. However, this institution was not subject to an enforcement action because they were proactive in rectifying the situation. Upon discovering what their loan officers were taking part in, the institution terminated them and self-initiated a remediation plan.

Administrative and Enforcement Changes

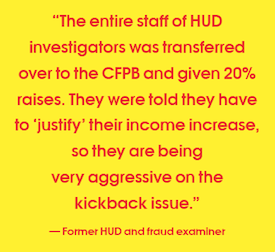

More prevalent than actual amendments or additions to the rules under Section 8, the CFPB implemented a number of changes in the way business is carried out by virtue of the agency enforcement actions. The CFPB is using such enforcement actions to convey to the industry that it means business. A former HUD investigator and fraud examiner commented, “The entire staff of HUD investigators was transferred over to the CFPB and given 20% raises. They were told they have to ‘justify’ their income increase, so they are being very aggressive on the kickback issue. In addition, they have hired more people in this department to investigate complaints and find violations.”

The CFPB is currently paying close attention to the individuals/small players, as well as the larger institutional mortgage companies. With respect to the small players, the CFPB is looking at the loan officer, real estate agent and developer. A common violation that these smaller firms or individuals commit, in addition to possible violations resulting from social media posts, stems from agreements among themselves.

An example of this is where a mortgage company owner is approached by a real estate agent to become an in-house lender, and, in turn, the agent demands a $60,000 set-up fee. This agreement would have allowed for an up-front payment for service not yet rendered, making it a violation of Section 8, and therefore would subject those individuals to fines and penalties.

In reviewing the larger full-service mortgage companies, the agency is reviewing the institutions’ actions, and imposing large fines to set an example.

The biggest enforcement trend that the CFPB is following regards the agreements between institutions and individuals in the mortgage industry. There are generally two types of agreements resulting in violations: lead-generation agreements and marketing service agreement.

Lead-Generation Agreements

A lead-generation agreement consists of just that, paying for leads. While paying for the lead is permitted under RESPA, paying for the results from the lead is not. For instance, a real estate agent can collect basic information (name, address, phone number, etc.) from a consumer and pass it on to a mortgage company. The mortgage company would then pay the real estate company for the lead — perhaps $50 or the current rate in the geographic area in which the lead is generated. What is not permitted, however, is for the mortgage company to first collect the lead, attempt to pre-qualify the consumer, and pay more than the agreed upon amount ($50) if it turns out to be a “better lead.”

A lead-generation agreement consists of just that, paying for leads. While paying for the lead is permitted under RESPA, paying for the results from the lead is not. For instance, a real estate agent can collect basic information (name, address, phone number, etc.) from a consumer and pass it on to a mortgage company. The mortgage company would then pay the real estate company for the lead — perhaps $50 or the current rate in the geographic area in which the lead is generated. What is not permitted, however, is for the mortgage company to first collect the lead, attempt to pre-qualify the consumer, and pay more than the agreed upon amount ($50) if it turns out to be a “better lead.”

Marketing Service Agreements

MSAs consist of agreements between companies in which marketing is provided to help refer business. In these agreements there must be marketing services performed before payment can be made. In addition, the company charging under the marketing service agreement has to prove the value of services, such as the advertising. When compared with lead-generation agreements, these MSAs are a more prominent focus under the CFPB and there is a growing trend of enforcement.

An example of enforcement of MSAs occurred in September 2014, when the CFPB entered into a Consent Order with Lighthouse Title, a Michigan title insurance agency, for entering into an MSA with real estate brokers with the agreement that such brokers would refer closing and title business to Lighthouse Title.

The CFPB found that the MSA made it seem as if the payments would be based upon marketing services that the real estate companies were to provide to Lighthouse Title. However, Lighthouse set the fees it would pay under the agreement to each company, and the fees Lighthouse paid to the real estate brokers was determined, in part, on the number of referrals or potential referrals Lighthouse would receive from those companies.

Under the MSA, this is a violation because the fees paid should have been on the fair value of marketing services actually rendered, rather than based upon the number of referrals or expected referrals they were to receive.

Because of this, the CFPB found that more business was referred to Lighthouse when a business was contracted under an MSA then when there was not such an agreement. Therefore, the CFPB penalized Lighthouse Title as follows:

Civil money penalty in the amount of $200,000

Prohibition of entering into MSAs in the future

Requirement to terminate all existing MSAs

For a five year period, requirement to document all exchanges of things of value worth $5.00 or more with persons in a position to refer business.

Affiliated Business Disclosures

Another area of review by the CFPB is disclosures between entities that are conducting business together pursuant to agreements. Such disclosures are called the Affiliated Business Arrangement Disclosures and provide a statutory safe harbor to companies to avoid Section 8 violations, if properly made. An AfBA disclosure must include the following:

A statement of the existence of the affiliated business relationship.

An explanation of the nature of the relationship among the parties, including an explanation of the referring party’s ownership and financial interests in the referred affiliated business entity.

An estimate of the charge or range of charges generally imposed by the referred affiliated business entity.

A statement that the consumer is not required to use the referred affiliated business entity and may elect to use any entity providing the requisite settlement services of his or her choice.

An acknowledgement line where the consumer must sign and date the disclosure as evidence of his or her receipt.

In May 2014, the CFPB filed a consent order with RealtySouth, the largest real estate firm in Alabama. The CFPB found that RealtySouth providedinadequate disclosures that could leave consumers unaware of their rights to choose service providers during the home buying process.

In May 2014, the CFPB filed a consent order with RealtySouth, the largest real estate firm in Alabama. The CFPB found that RealtySouth providedinadequate disclosures that could leave consumers unaware of their rights to choose service providers during the home buying process.

The penalties imposed on RealtySouth were as follows:

$500,000 civil penalty

Must ensure its disclosures comply with RESPA

Ensure that its employee training materials emphasize its agents cannot require the use of affiliates.

Recommendation of Risk Management Program

With the increase on enforcement by the CFPB and the increased scrutiny on social media, financial institutions need to consider the implementation of a risk management program to identify, monitor and control risks related to RESPA Section 8, the social media guidelines and the use of social media sites. The size of this risk management program should correlate with the amount of involvement and investment in social media by the company or individual. The guidance states that the program should be developed in collaboration with specialists in compliance, legal, technology, information security, human resources and marketing. It also stated components of a risk management program to include the following:

A governance structure with clear roles in which the board of directors or senior management directs how using social media contributes to goals of the company.

Policies and procedures regarding use and monitoring of social media and compliance with all applicable consumer protection laws and regulations.

A risk management process for selecting and managing third-party relationships in connection with social media.

An employee training program which incorporates policies and procedures for official use of social media.

An oversight process for monitoring information posted to social media sites administered by the institution or a contracted third party.

Audit and compliance functions to ensure ongoing compliance with the institution’s social media policies and procedures.

Parameters for providing appropriate reporting to financial institutions’ board of directors or senior management of the effectiveness of the social media program and if the stated objectives are being achieved.

When HUD passed on supervisory powers to the CFPB, there were modifications to RESPA, specifically including guidance regarding social media. However, the biggest change that arose was in the field of enforcement.

The CFPB has sent a message to the mortgage industry through the use of hungry investigators. It is also following the trend of bringing down the hammer on those companies in the industry that fail at full compliance with RESPA, resulting in unsavory business practices — contrary to the primary goal of Section 8, which is and will continue to be aimed at the protection of the consumer.