New Data Reveals Implementation Challenges Under FinCEN Rule

April 9, 2026

Significant operational strain, widespread uncertainty and growing concern defined the title industry’s experience under FinCEN’s Residential Real Estate Rule, according to a new survey from ALTA. The findings reveal that, while companies worked to comply, the rule introduced complex requirements that disrupted workflows, created friction with consumers and raised fundamental questions about responsibility and risk.

Significant operational strain, widespread uncertainty and growing concern defined the title industry’s experience under FinCEN’s Residential Real Estate Rule, according to a new survey from ALTA. The findings reveal that, while companies worked to comply, the rule introduced complex requirements that disrupted workflows, created friction with consumers and raised fundamental questions about responsibility and risk.

Drawing responses from nearly 1,300 professionals nationwide, the survey captures a cross-section of title agents, underwriters, attorneys and settlement providers working across a range of markets and transaction volumes.

The rule was paused March 19 when a judge in the Eastern District of Texas issued a ruling holding that FinCEN exceeded its statutory authority under the Bank Secrecy Act and ordered the rule be set aside. Following the court’s decision, FinCEN posted an alert on its website that said “reporting persons are not currently required to file real estate reports with FinCEN and are not subject to liability if they fail to do so while the order remains in force.”

ALTA wanted to use this time to collect information about how the rule had impacted operations. While many companies took steps to comply with the rule, the survey shows there was no single approach to implementation. Some organizations relied on third-party vendors (42%) or software platforms (22%), while others handled reporting internally (36%), often requiring new processes and workflows.

At the same time, not all companies had dedicated staff assigned to manage reporting, highlighting the challenge of absorbing new regulatory responsibilities within existing teams. About 55% had a dedicated staff to handle reporting. The survey could not capture the average time to collect and report the needed information due to a wide range resulting in different ways to handle rule compliance.

For many respondents, the rule introduced a level of complexity that extended well beyond filing reports.

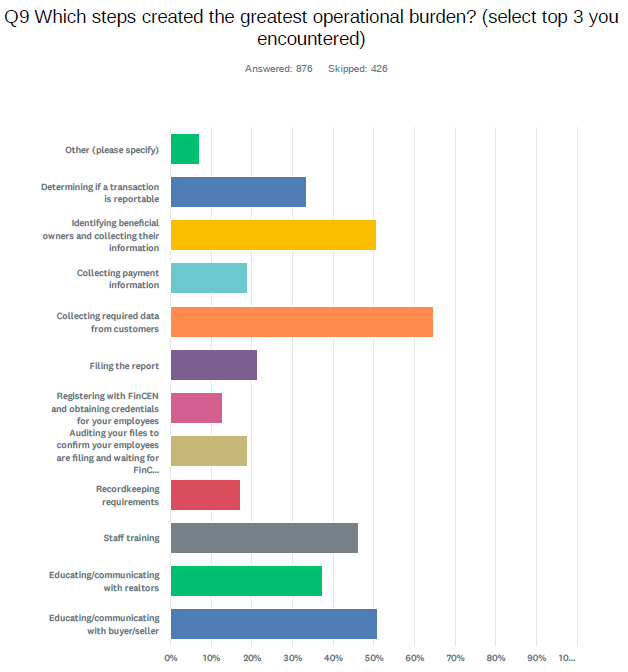

Where the Burden Was Felt Most

Survey responses point to several consistent pressure points in the reporting process. Among the most significant challenges were:

- Collecting required data from customers

- Identifying beneficial owners and collecting their information

- Educating/communicating with buyer/seller

- Staff training

- Educating/communicating with Realtors

- Determining if a transaction is reportable

These steps were not just procedural. Many respondents described them as disruptive to normal workflows and difficult to integrate into the fast-paced nature of real estate transactions.

“The complete transaction is a burden,” one respondent noted, while another said, “every one of these steps created an operational burden.”

Another respondent said they spent hundreds of hours modifying their title production system to help identify transactions and also collect the needed information.

Friction With Consumers and Counterparties

Beyond internal operations, the survey highlights significant friction with buyers, sellers and other transaction participants. Respondents frequently cite:

- Difficulty obtaining sensitive financial and personal information

- Resistance from consumers concerned about privacy

- Challenges explaining the purpose and scope of the rule

- Delays caused by incomplete or late information

According to the survey, about 66% of those surveyed said transactions were delayed due to the reporting requirements. Buyers or sellers expressed significant concerns about privacy/data security (85%), as well as delays in the transaction (58%). Meanwhile, 45% of buyers or sellers refused to provide necessary information for reporting.

In some cases, the timing of information requests created additional complications.

“At the beginning of the transaction, no one knows the payment information,” one respondent said. “At the end, collection feels like a surprise. It's an operational and expectation management nightmare.”

These challenges underscore the tension between regulatory requirements and the realities of consumer behavior during a transaction.

Uncertainty and Lack of Clarity

A recurring theme throughout the survey is uncertainty, both in how the rule should be applied and what information was required. Respondents pointed to ambiguity in determining reportable transactions, confusion around terminology and requirements and limited guidance for complex or non-standard scenarios.

“Too much is left to the reporter to interpret,” one participant noted.

This lack of clarity often translated into additional time, training and risk for companies trying to ensure compliance.

Questions of Responsibility and Risk

Perhaps the most consistent feedback centered on who should bear responsibility for reporting. Many respondents expressed concern that the rule placed disproportionate burden and liability on title and settlement professionals. These are parties that do not control the underlying financial activity being reported.

“We are not forensic accountants or tax professionals,” one respondent wrote. “We are being asked to collect information that is none of our business.”

Others questioned whether financial institutions or transaction participants themselves would be better positioned to handle reporting obligations.

Calls for Change

While perspectives varied, many respondents suggested similar areas for improvement, including:

- Narrowing the scope of reportable transactions

- Establishing clear thresholds

- Reducing the amount of required data

- Providing clearer guidance and definitions

- Reconsidering who is responsible for reporting

Some respondents supported the broader goal of combating illicit finance but emphasized the need for a more practical, targeted approach.

The survey results come at a pivotal moment. While the court ruling vacated the rule for now, its future remains uncertain as legal and policy discussions continue. For ALTA, the findings provide a critical foundation for ongoing advocacy to help ensure policymakers understand not just the intent of the rule, but how it functions in practice.

ALTA Advocacy

ALTA continues to engage with FinCEN, monitor legal and regulatory developments and keep you informed as this situation evolves. ALTA is pushing for more clarity around the rule and urging that any future changes come with adequate notice and a reasonable implementation period.

ALTA submitted a letter to FinCEN Director Andrea Gacki outlining recommendations to reduce the Rule’s burden on title professionals. Specific changes ALTA would like FinCEN to make to the rule include:

- Impose a nominal dollar threshold, as included in other anti-money laundering regulations, to exclude gratuitous and low-value transfers and focus reporting on higher-value transactions.

- Exempt transfers from a seller to an entity the seller controls, such as a single-member LLC or revocable living trust, which represent a change in the form of title not beneficial ownership.

- Exempt transfers that are the result of foreclosure proceedings, whether judicial or otherwise.

- Limit payment information collection to what settlement agents can realistically obtain, such as information available on a wire transfer receipt or on the face of a check.

- Eliminate seller and transferor information collection. Collecting seller tax identification numbers and financial details adds significant workflow burden while its law enforcement value remains unclear.

Get Involved

- Register for the ALTA Advocacy Summit (May 11-13) for your chance to meet directly with lawmakers and their staff to discuss the burden of rule.

- Join the Title Action Network to make sure you’re responding to developments around the FinCEN rule or weighing in on pending legislation or regulation.

Contact ALTA at 202-296-3671 or [email protected].