Eight Details About SBA’s Paycheck Protection Program

March 31, 2020

One of the central pillars of the $2 trillion COVID-19 stimulus package known as the CARES Act is nearly $350 billion for forgivable loans to help small businesses with payroll costs and avoid layoffs. The program called the Paycheck Protection Program is run by the federal Small Business Administration. Guidelines for the program will be released this week.

As title and settlement companies assess their options talking with their banker should be high on the list. The SBA has a network of 1,800 approved lenders. Because there is limited funds, title companies should speak to an SBA lender as soon as possible if there are concerns about retaining staff and paying other expenses. Contact your bank to see if it is an SBA-approved lender. Your current banker likely already knows your business and will be able to help you navigate the application process. If it is not an SBA-approved lender, here is the list of the top 100 SBA lenders.

Click here to access the application for the Paycheck Protection Program. The application includes instructions for completing the form. Submit the application to an SBA participating lender.

Here are eight things you should know as you talk to your banker about a Payroll Protection Program loan.

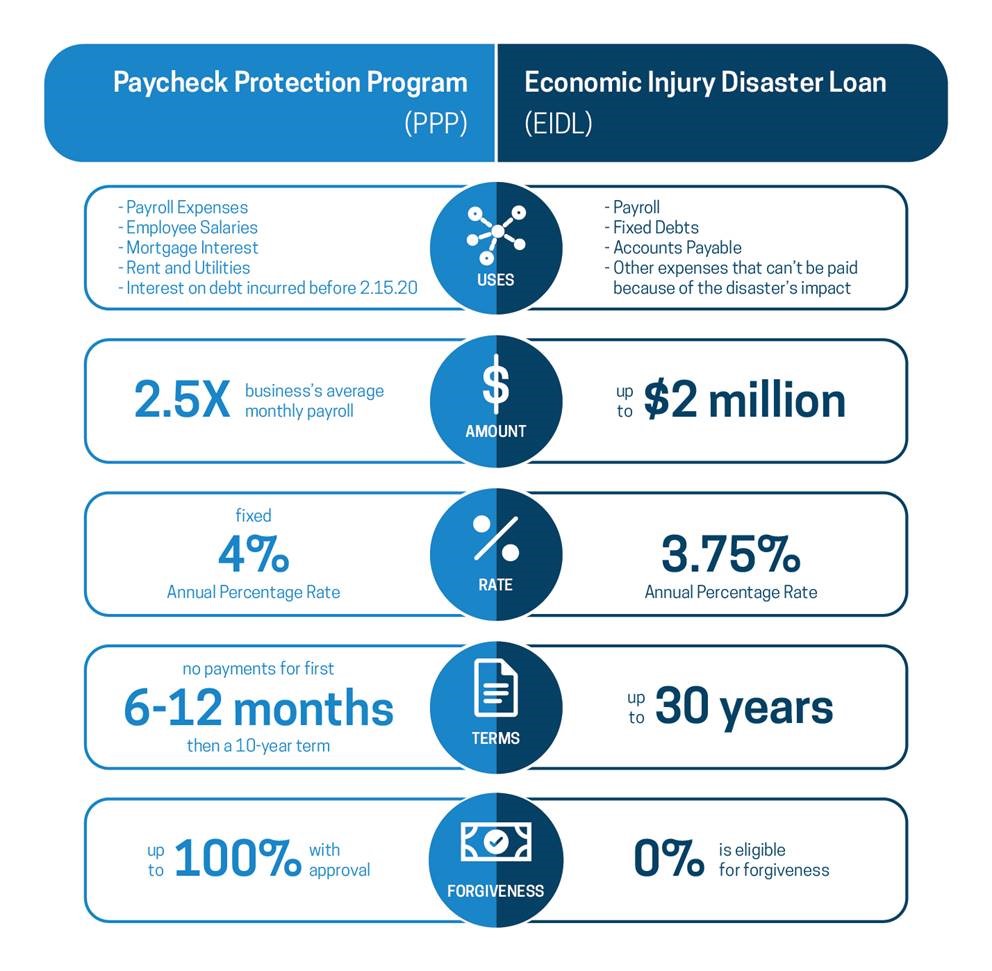

- Who is eligible: Any business that was in operation before February 15, 2020 with 500 or less employees OR $12m or less in gross revenue for title agents ($41.5m for title underwriters). Note, if you have multiple title companies or operate with a series of joint ventures you may need to aggregate employees and revenue for all operations.

- How much can you borrow: Up to 250% of the average monthly payroll cost from the previous 12 months. The maximum loan amount is $10m. To determine the amount you might be eligible to borrow, take all your payroll expenses and multiply that by 2.5. The average monthly compensation of an individual employee or owners is capped at $8,333.33 per month which equates to an annualized salary of $100K. For example, if your average payroll is $100,000 a month then the most you can apply for is $250,000.

- What payroll expenses can I use to determine by loan amount: Employee salaries, tips, sick or vacation pay, sick or parental leave, health care costs, retirement benefits (401k match) and state or local payroll taxes. It’s important to remember that the owner can include their income as well in this calculation. For individuals whose salary is included in the calculation, the salary is limited to the first $100,000 in annual income.

- How can I use the loan proceeds: You can use the loan proceeds to cover payroll costs, rent, utilities, health insurance, paid sick leave, and mortgage interest payments (although not mortgage principal) on your office locations.

- Will some amount of these loans be forgiven: Yes. The SBA will forgive repayment of PPP loan proceeds equal to the amount use to fund payroll, mortgage interest, rent and utility payments for the 8 week period starting from the loan origination date. If you layoff workers or reduce wages after obtaining a loan, the amount eligible for forgiveness will be reduced.

- What about the amounts not forgiven: Any amount not forgiven by the SBA is repayable as a 10 year loan at a rate not to exceed 4 percent.

- Do I have to have already laid off workers to be eligible: No. The goal of these loans is to help avoid layoffs or salary reductions.

- What documents do I need to provide my lender: Guidelines will be published this week to know what documentation you need to provide to get a PPP loan. There are no collateral requirements for these loans or personal guarantees.

There are also other options and emergency disaster loans and grants for businesses:

- Economic Injury Disaster Loans and Loan Advance: In response to the COVID-19 pandemic, small business owners in all U.S. states, Washington D.C., and territories are eligible to apply for an Economic Injury Disaster Loan advance of up to $10,000.

- SBA Express Bridge Loans: This allows small businesses who currently have a business relationship with an SBA Express Lender to access up to $25,000 with less paperwork. Terms include up to $25,000, fast turnaround and will be repaid in full or in part by proceeds from the EIDL loan. Find an Express Bridge Loan Lenderby connecting with your local SBA District Office.

Contact ALTA at 202-296-3671 or [email protected].